Home loan interest rates have started to drop following a series of repo rate cuts by the Reserve Bank of India (RBI). In the first six months of the year, the repo rate was reduced by 100 basis points (bps) from 6.5% to 5.5%. When the central bank lowers the repo rate, it typically results in lower interest rates for home loans. This change allows home loan borrowers to save a significant amount on interest payments. But how much will you save? That depends on your home loan interest rate regime and how much your lender is willing to pass on the benefits to you. If all this seems complicated, don’t worry. We are here to help home loan borrowers understand this better so they can take full advantage of the benefits from these repo rate cuts.

Like what you’re reading?

Get our latest, straight to your inbox.

MCLR or RLLR: Which is your home loan rate regime?

Typically, your home loan interest rate is tied to a benchmark, which depends on when you took out the home loan. For those who took their home loans between July 1, 2010, and March 31, 2016, the interest rates are typically based on the base rate. From April 1, 2016, to September 30, 2019, home loans are usually linked to the Marginal Cost of Funds Based Lending Rate (MCLR). Since October 1, 2019, the Reserve Bank of India (RBI) has mandated that lenders link all new floating-rate loans to the External Benchmark Lending Rate (EBLR). For most banks and housing finance companies, this external benchmark is the repo rate, which is why it is often referred to as the Repo Linked Lending Rate (RLLR).

As of December 2024, approximately 61% of existing floating-rate loans are linked to the repo rate, according to the RBI’s Annual Report 2025. About 36% of loans are tied to the MCLR, while 3% are linked to other benchmarks. In this blog, we are discussing MCLR and Repo Linked Lending Rate, which is a type of External Benchmark Lending Rates.

Difference between MCLR and Repo Linked Lending Rate

The Marginal Cost of Funds Based Lending Rate (MCLR) represents the lowest rate at which banks can lend funds to borrowers. Under this loan regime, the interest rate is typically set as MCLR plus a spread determined by the bank, which depends on the borrower’s credit risk and other factors. It serves as an internal benchmark, where the bank sets interest rates based on its cost of funds. Factors such as banking system liquidity, operating cost and low-cost deposits also affect it.

In the case of the Repo Linked Lending Rate, the benchmark is the repo rate. The repo rate is the interest rate at which commercial banks borrow money from the Reserve Bank of India. Banks typically apply a spread over the repo rate to determine the interest rates for loans that fall under the RLLR.

As these are floating-rate loans, the interest rate is reset automatically without any additional cost to the borrower.

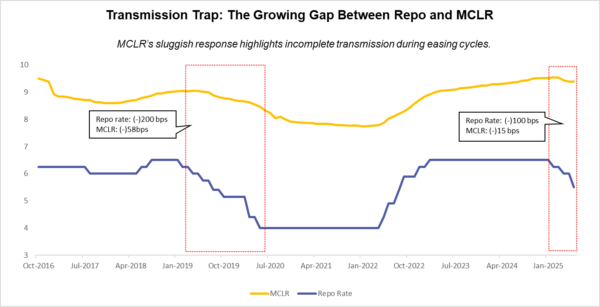

The main difference between MCLR and RLLR lies in the time it takes to reset the loan interest rate and pass on the benefits to borrowers. The MCLR is reset periodically, depending on the bank’s policy, which results in a comparatively slower transmission of repo rate changes, as it is not directly linked to them. Lenders typically take 6 to 12 months to revise the MCLR rate.

Check how MCLR rates have been adjusted so far in 2025

Source : 1 Finance research, June 12, 2025

In contrast, banks must reset the interest rate under the Repo Linked Lending Rate at least once every three months. Consequently, the transmission of Repo Linked Loan Rates typically occurs within a short span of a repo rate change. Because RLLR is directly tied to the repo rate, it offers greater transparency and a more immediate reflection of changes.

So, the transmission of rate cuts by the Reserve Bank of India will be passed on to borrowers quickly through the Repo Linked Lending Rate. In contrast, the transmission of rate cuts under the MCLR is slow, and it usually takes time before the actual benefits are finally passed on to the borrower.

MCLR vs. Repo Linked Lending Rate: Know the difference

| Parameter | MCLR | RLLR |

|---|---|---|

| Benchmark | Banks internally decide their own benchmark | External, typically linked to repo rate |

| Reset period | Varies from bank to bank, usually 6-12 months | Quarterly |

| Transparency | Moderate | High |

| Transmission rate | Slower | Faster |

| Interest rate change | Gradually, depending on banks’ internal costs and policy | Frequently, as and when repo rate is changed |

For instance, if you have an outstanding home loan balance of ₹25 lakh and your loan is under the MCLR regime, you are currently paying an interest rate of 9% per annum with 15 years remaining to repay the loan. If you switch your loan regime to the Repo Linked Lending Rate, your home loan will be reduced to 8.5%, effective immediately.

In such scenario, check how much home loan EMI you will save by switching your home loan interest rate regime

| Parameter | Home loan under RLLR | Home loan under MCLR |

|---|---|---|

| Loan Amount (₹) | 25,00,000 | 25,00,000 |

| Rate of interest (%) | 9 | 8.5 |

| Tenure (months) | 180 | 180 |

| EMI | 25,357 | 24,618 |

| Monthly EMI saved (₹) | 739 | |

| Annual EMI saved (₹) | 8,868 | |

| Total interest saved (₹) | 1,32,872 |

You can calculate the change in your home loan EMI using our calculator Floating Interest Rate Calculator

How to switch your home loan interest regime

The process of changing your home loan interest regime is quite simple. All you need to do is inform your bank that you wish to switch to a different loan interest regime. However, keep in mind that banks often charge a fixed fee for converting your home loan from one regime to another.

For example, according to HDFC Bank, you will incur a conversion fee of 0.25% of the principal outstanding amount (plus applicable taxes) or ₹5,000 plus applicable taxes, whichever is lower. Different banks have different rules regarding this fee. Once you request the conversion and pay the fee, it typically takes 7 to 15 days to process, depending on the bank’s internal loan approval process.

Not all banks passed repo rate cuts to borrowers

One more thing to remember is whether the bank is passing on the benefit of the repo rate cut to home loan borrowers. According to 1 Finance Research, the average rate change in public sector banks is 70 basis points, while in private sector banks, it is 15 basis points as of June 12, 2025.

Check how banks, lenders have passed on the repo rate cut to home loan borrowers so far in 2025

| Category | Average Rate Change (bps) | Transmission Quality |

|---|---|---|

| Public Sector Banks | -70 | Excellent |

| Housing Finance Companies | -40 | Good |

| Private Banks | -15 | Poor |

| NBFCs | 0 | No transmission |

| Small Finance Banks | 0 | No transmission |

Source: 1 Finance research, June 12, 2025

Key things to check before you switch your home loan regime

Before rushing to convert your home loan interest rate regime, you should check a few things:

- Is your lender offering any loan regime that is directly linked to the repo rate? The name may vary, such as External Benchmark Lending Rate, Repo Linked Lending Rate, or Repo Based Lending Rate (RBLR). The underlying benchmark should be linked to the repo rate.

- If the bank is offering it, how much of the repo rate cut have they transmitted so far? The RBI has reduced the repo rate by 100 basis points, so how much has your bank adjusted?

- Once you have the revised interest rate that will apply to you, conduct a thorough cost-benefit analysis to understand how much you will save on home loan interest. Be sure to factor in the conversion fee.

- If your bank is not offering an interest rate linked to the repo rate, you might consider transferring your home loan to another bank. Again, you should do a detailed calculation to determine the actual savings before making the switch.

If you are unsure about your potential savings, consult a Qualified Financial Advisor who can handle the calculations and other considerations for you, guiding you to the most beneficial loan regime.