Over the past decade, the cost of education in India has shot up dramatically, changing the way parents think about investing in their child’s future. It starts right from school—especially in big cities—where tuition fees keep climbing by about 7% to 15% each year. By the time a child finishes school, the fees may reach as high as ₹1.68 crore in some elite schools. The highest average tuition cost for an elite school is ₹76.2 lakh for KG-12, according to 1 Finance Research.

Like what you’re reading?

Get our latest, straight to your inbox.

And higher education isn’t any easier on the pocket. Today, the cost of higher education really shows how wide the affordability gap has become.

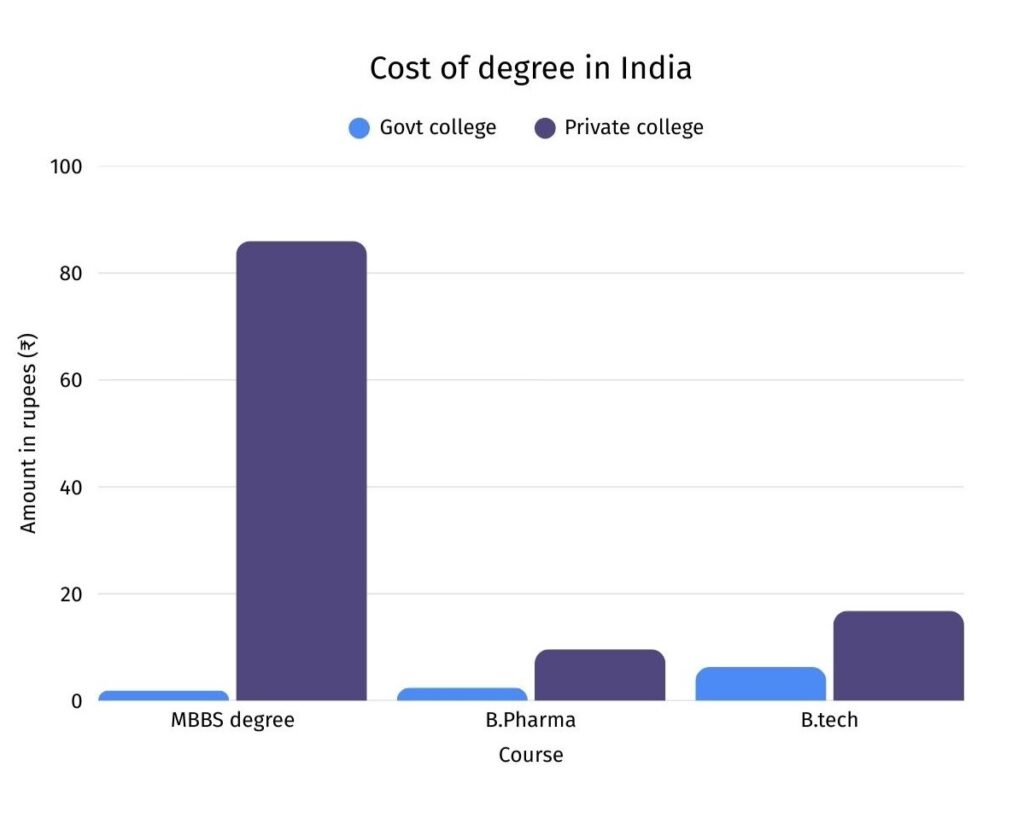

For example, a 5-year MBBS degree at a government college costs around ₹1.9 lakh. But in a private college? The same degree can cost as much as ₹82 lakh—that’s nearly 42 times higher.

And it’s not just medicine. Courses like B.Tech or B.Pharm follow the same trend, where private colleges charge three to four times more than government institutions, putting an ever-growing financial strain on families across the country.

On top of rising tuition fees, families also have to pay more each year for things like books, coaching classes, and transport—these costs often go up by 7–9% every year.

With education now seen as both essential and a big long-term investment, families have been forced to rethink their finances.

This has pushed household spending on education through the roof—jumping 4.6 times, from ₹1.8 lakh crore in FY12 to ₹8.43 lakh crore in FY24. On an individual level, the average spend has also shot up—from about ₹1,500 per person back then to an expected ₹6,100 by 2026.

While some can afford it, many can’t.

This makes them turn to borrowing money. Here’s the most telling evidence:

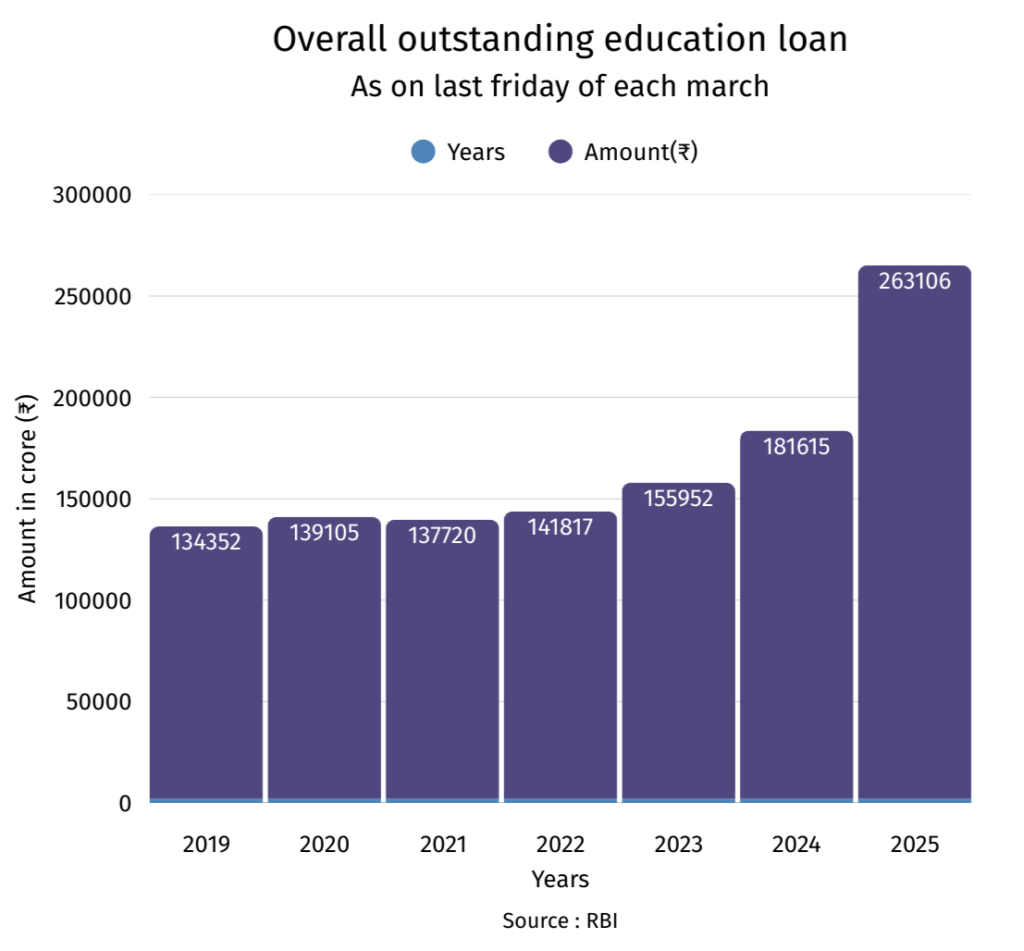

According to RBI data, between March 2019 and March 2025, there has been a 95.83% increase in outstanding education loans in absolute terms.

According to ministry of finance, in the financial year 2023-24, Public Sector Banks in India disbursed education loans to 7,36,580 students, up from 6,29,594 in 2022-23, marking a 17% annual growth in the number of loan accounts;

The sharp rise in education loans tells a tough story: for many Indian parents, borrowing is a lifeline. As school and college fees climb faster than family budgets can handle, loans have become less of a fallback and more of a necessity. Parents are seen increasingly leaning on borrowed money to fill the gap between dreams and affordability.

Educational loan scenario in India vs. in US and UK

India’s education loan boom mirrors worrying trends seen in advanced economies. In the US, student debt has crossed $1.8 trillion, while in the UK it has exceeded £200 billion, with mounting repayment complexities and significant economic consequences.

In India, households already spend nearly 33% of their income on EMIs. Adding education loan repayments to this burden could amplify socioeconomic stress over the coming decades.

As in the West, heavy debt burdens can delay milestones such as homeownership and retirement, while also deepening inequality. Without timely reforms or stronger financial aid structures, India risks facing similar long-term challenges.

The early warning signs are already visible. By 2024, the education loan category under personal loans recorded the highest NPAs (in SCB) , underscoring both repayment challenges and systemic risks.

A critical difference, however, lies in who bears the debt burden. In the US and UK, students are primarily responsible for repayment. In contrast, in India, education loans often become household liabilities, as parents usually take responsibility for repayment.

This reflects India’s family-centric culture, where parents prioritize their children’s education and success, even at the cost of long-term financial strain.

Key things you need to keep in mind while taking an education loan

Before committing to an education loan, it’s genuinely wise for parents and students to first consult a financial advisor. A professional brings expertise and an unbiased perspective to evaluate how taking a loan will affect your household finances and create a repayment strategy aligned with career prospects.

Alongside this, consider these steps for financial safety and peace of mind:

- Plan early: Research lenders and required documents about 12 months before admission, but only apply after receiving admission to ensure correct loan amount and smooth processing.

- Check collateral-free loan limits: Banks typically offer ₹15-20 lakh for studies in India and ₹20–50 lakh for studies abroad without collateral. Make a list of your preferred institutions and check their specific loan limits with different lenders to optimize your borrowing capacity

- Use the Vidya Lakshmi Portal effectively: This government initiative is a game-changer that allows you to compare 84 different loan schemes from 38 participating banks through a single application. The portal enables you to apply to up to three banks simultaneously, saving significant time and paperwork. Register early on www.vidyalakshmi.co.in, and take advantage of the portal’s tracking system to monitor your application status in real-time.

- Understand loan terms: Aim for interest rates between 8–12%, with a repayment period of 10–15 years for manageable EMIs.

- Manage EMI burden: Keep monthly EMIs under 20–25% of household income to avoid undue financial stress.

- Maximise tax benefits: Deduct the full interest paid under Section 80E for up to 8 years—no upper limit on the deduction.

Education loan to study in India

If you’re considering a domestic education loan for studies within India, you’ll find the process is generally straightforward and family-friendly. Most major banks and NBFCs now offer collateral-free loans for up to ₹15–20 lakh, which means you won’t need to pledge property or other assets for a typical undergraduate or postgraduate degree at a recognized Indian institution.

These loans usually come with attractive interest rates—often between 8% and 12%, depending on your profile and the lender—plus flexible repayment periods that stretch from 10 to 15 years, keeping monthly payments manageable. Approval and processing are relatively quick for admissions to accredited colleges or universities, and the documentation required is clear and streamlined.

One of the biggest benefits for parents is the tax deduction on interest payments under Section 80E, available for the first 8 years of loan repayment—there’s no upper limit, so every rupee of interest qualifies for relief, making this a smart way to ease the financial load.

All things considered, a domestic education loan is a practical, cost-effective solution for most students aiming for reputable institutions in India, balancing flexibility and affordability while offering meaningful relief through tax benefits.

Education loan to study abroad

Did you know that more than 1.8 million Indian students are now studying overseas, according to the Ministry of External Affairs? That’s a dramatic rise and, as the Crisil industry report for 2024 points out, overseas education loans now make up 57% of all education loans taken by Indian families as of December 2023.

When you’re thinking about a foreign education loan, you’re looking at much higher tuition and living costs compared to studying in India.

The good news is many banks now offer collateral-free loans of up to ₹50 lakh for top international universities, making global dreams far more accessible. But keep in mind, these loans often come with extra strings attached, such as a co-signer, proof of admission, and paperwork tied to your visa or your course expenses.

Interest rates for studying abroad can be a bit higher than for domestic loans and there’s always the added uncertainty of currency fluctuations, which can impact how much you actually end up paying.

On the flip side, some banks and NBFCs have started tailoring their loan products specifically for overseas courses at prestigious programs, which can open doors through easier eligibility and application processes.

Still, it’s absolutely essential to take a hard look at the full cost—including tuition, travel, insurance, and that all-important exchange rate—before taking the plunge on a foreign education loan. Thoughtful preparation here will keep surprises to a minimum and set you up for the richest experience possible abroad.

Bank vs. NBFC: Which one should you choose for an education loan?

If you’re exploring education loans in India, it’s helpful to know how banks and NBFCs each approach student financing. Banks often come with lower interest rates and thorough eligibility checks, while NBFCs are known for quicker approvals and more flexible coverage—even for courses outside the usual lists.

| Feature | Banks | NBFCs |

|---|---|---|

| Courses covered | Specified courses at pre-approved list of colleges | Greater coverage: part-time, online, correspondence, no specified list/grading |

| Loan coverage | Tuition, travel, exam fees, lab fees, capping on other related costs | 100% loan coverage: tuition, travel, uniform/books/equipment, exam fees |

| Underwriting model | Traditional collateral-based lending | Specialized, based on institution, employability of student, earning co-borrower |

| Turnaround time (TAT) | 15–20 days | 3–7 days |

| Processing fees | Low (up to 1% or min Rs 10,000 for loans above Rs 20 lakh) | Moderate (1%–2% of loan amount) |

| Interest rates | Low (8.0%–12.5%) | Moderate (12.0%–15.0%) |

| Collateral | No security up to Rs 0.75 million; tangible collateral above Rs 0.75 million | Majority unsecured; for secured—tangible (house), intangible (FD, life insurance) |

| Average loan ticket size | Lower (Rs 0.5–0.6 million) | Higher (Rs 2–3 million) |

| Margin | Up to Rs 0.4 million: Nil; Above Rs 0.4 million: Domestic – 5%; Abroad – 15% | Higher loan coverage |

| Repayment period | Max 15 years after course period + 12 months repayment holiday | Max 10–15 years including course period and grace period |

| Repayment options | Fixed, no customization | Customization; multiple options (interest/partial interest during course, EMI after course/moratorium) |

| Sourcing channels | DSAs, branch walk-ins, education institutions, digital channels, counselors | Diversified: educational institutions, counselors, consultants, test prep centres, DSAs, student visa consultants, digital |

Why financial planning matters while taking education loan

It’s honestly not enough to just get approved for a loan and hope for the best—education costs don’t just cover tuition, but also living, hostel, and exam expenses, all of which can creep up faster than you expect.

If you don’t plan for at least 12–15% annual inflation (which is typical for top courses), those costs can balloon, and you could end up borrowing more than you really wanted—or worse, find yourself scrambling midway through a course.

A well-structured plan lets you know exactly how much you’ll need and helps you avoid taking on unmanageable debt. If you set up a systematic investment plan, scout for scholarships early, and revise your savings every couple of years, you stay ahead of surprises.

Most importantly, when you’ve got a plan, you aren’t stuck worrying about finances in the middle of your child’s studies. So, financial planning is what turns an education loan from a potential burden into a strategic step toward your goals.

To make sure your education loan truly supports your child’s dreams—without creating future financial stress—it’s smart to have a conversation with a Qualified Financial Advisor. Connecting with an an advisor today means securing your child’s tomorrow with clarity and peace of mind.